According to Federal Reserve research, as many as 30% of adults attend college, with 4 out of 10 taking out loans to pay for at least some of their education. Just 21% of borrowers have redeemed their sums on the $1.78 trillion in total outstanding federal and private student debt, according to official data. Additionally, those who hold federal loans must start making payments in October after a hiatus since 2020. According to experts, most of you can repay your student debts on schedule if you use the appropriate tactics.

Tips on how to get out of student loans. (Source: Sofi Learn)

Quick Way to Pay Student Loans

There are strategies you may use to manage your balance if that October deadline is making you anxious. The most crucial step, according to WalletHub analyst Jill Gonzalez, is learning how to handle debt if you find yourself with a lot of it. First, strive to prevent delinquency by making at least the minimum monthly payment. Next, take into account your lifestyle and make an effort to reduce your spending on luxury things like subscriptions, high-priced phone bills, or delivery services.

Here’s a quick overview of the many ways you might repay debts quickly; scroll down for additional information on each of these ideas.

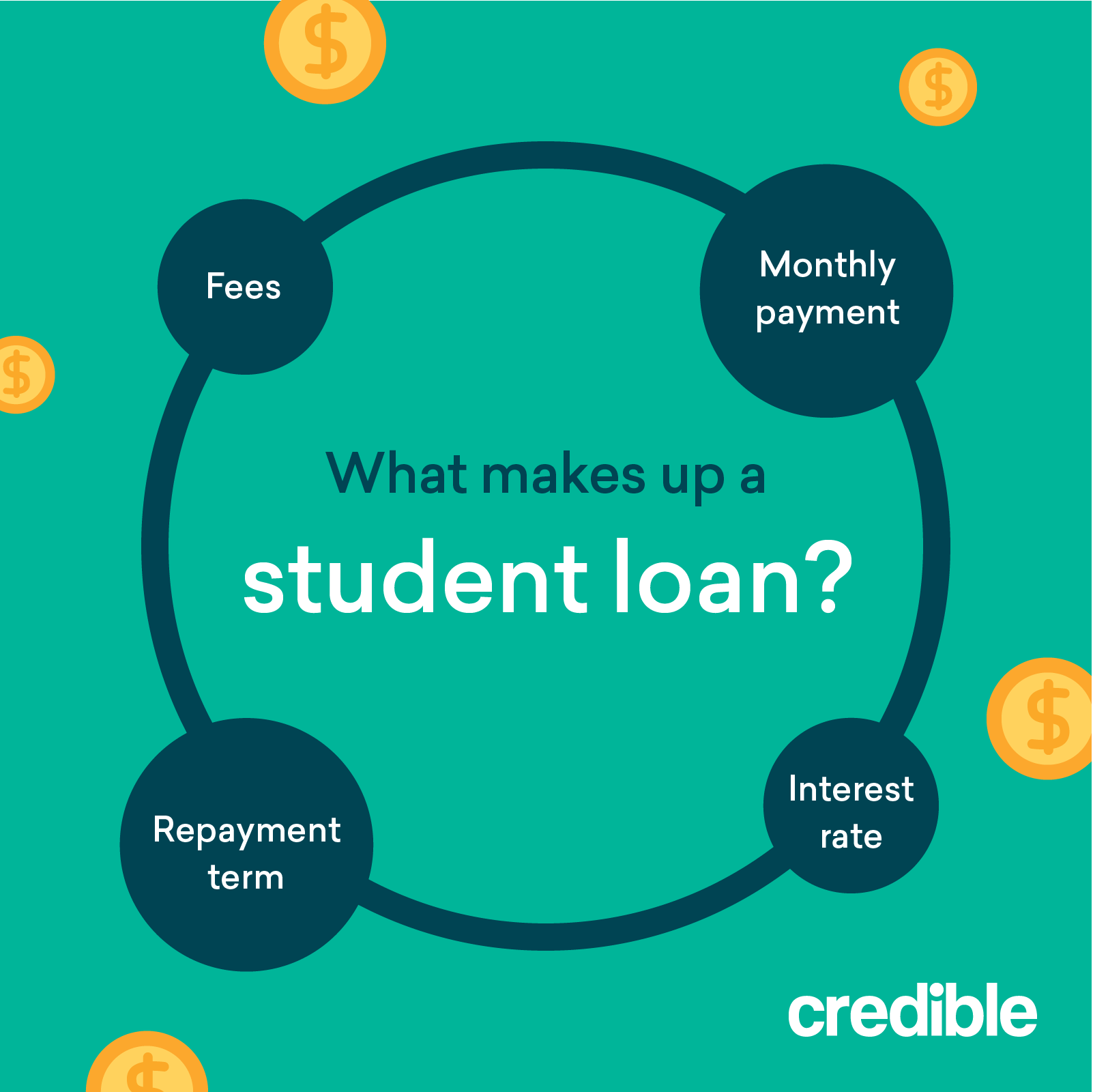

- Obtain details regarding the size, interest rate, and repayment choices of your loan.

- Set up a budget.

- Problem-solve with payment

- Think about refinancing

- Put loan payback first.

- Think about increasing your loan repayments.

- Use programs that provide help with loan repayment.

- Increasing debt repayments

- Stay persuaded

Obtain details regarding the size, interest rate, and repayment choices of your loan. When it comes to paying off this debt, time is of the essence. Servicers must wait a minimum of 90 days before reporting late payments for federal student loans. According to NerdWallet research, they can disclose late payments for private student loans in as little as 30 days.

This is referred to as delinquency if it eventually leads to a report to credit bureaus, and it can remain on your record for seven years. The longer the delinquency, the more damage it will do to your credit score. To prevent this, you must first be aware of the amount you owe, the interest rate, and the terms of your repayment obligations.

READ ALSO: Student Loan Payments Resume Could Hurt Housing Market

Find Out How Much You Owe in Student Loan Debt

On the Federal Student Aid website, it is quite simple to find out how much you now owe if you have federal loans. The Department of Education oversees this website, which compiles all of your loan information into one clear location. You can check the original loan amount, outstanding student loan balance, interest rate, and payment status here.

You’ll probably need to go to your servicer’s website or app to get private loans. You can phone them if you don’t know where to look for this information. If it doesn’t work, speak with the financial aid office at your school or check your credit record to find out how much you’ve borrowed and who is now servicing your loans.

How to determine the type of student loan repayment plan you are currently on Here are some of the most typical alternatives for paying back federal student loan debt:

- Standard Repayment Schedule: Fixed payments with a 10-year payoff period are anticipated.

- Graduated Repayment Plan: Over the loan’s 10-year term, payments rise gradually.

- Extended Repayment Plan: These payments may be set or graduated, and the loan balance may be repaid over 25 years. Although it may cost you more in interest, this choice can be the best one for people who want to make smaller monthly payments over a longer period.

- Pay As You Earn Payback Plan (PAYE): Based on discretionary income, this payment schedule never goes over what you would pay under a typical payback schedule.

- Saving on a Valuable Education (SAVE) Plan: The new SAVE Plan eliminates all outstanding interest for both subsidized and unsubsidized loans upon a scheduled payment, replacing the Revised Pay As You Earn Repayment Plan (REPAYE). Check the website for further details as more advantages are anticipated to take effect next summer.

- Income-based Repayment Plan (IBR): Depending on your income at the time it was opened, this payment plan maybe 10% or 15% of your discretionary income.

- Income-Contingent Repayment Plan (ICR): For the ICR plan, your monthly payments are equal to 20% of your discretionary income or the amount you would pay over 12 years on a set payment schedule.

- Income-Sensitive Repayment Plan: These monthly payments must be made within 15 years and are based on your yearly income.

If you’re unsure of the current plan you have, you can ask your loan servicer or visit the My Federal Student Aid website for more information.

Private student debt repayment is a little bit simpler. Some of the most popular possibilities to think about with this kind of loan are listed below:

- Immediate repayment: If you choose this option, you’ll start making full monthly payments even whilst you’re still in school.

- Only pay interest on your loan during the time you are in school if you choose the interest-only repayment option.

- Partial interest repayment: In this case, you will only be required to make fixed monthly payments that cover the interest part of your loan while you are still in school.

- In this scenario, which is probably the ideal choice for busy college students, you would postpone all payments until after you have finished your studies.

- Ask your loan servicer for more details if you are unsure which one you have or if you want to amend your repayment plan. They should be able to assist you in locating the ideal choice for your circumstances.

Gonzalez advises creating a thorough budgeting strategy as the greatest way to reduce the potential burden rather than worrying about your newly acquired debt responsibility. Gonzalez advises “considering your lifestyle and trying to cut out the luxury items from your expenses, such as subscriptions, expensive phone bills, or delivery services,” adding that “this allows you to put some money aside and build a debt payoff budget, which helps you determine how much you can allocate monthly to paying down your debt and how fast you can do it.”

According to a recent Wall Street Journal article, there are four essential phases to creating a plan:

- Make a list of all student loans, grants, scholarships, parent contributions, permitted credit card debt, and any personal income you may have to get a clear picture of your finances. This will help you determine how much money you have and where it is coming from.

- Determine the cost of attending college, including tuition, books, food, transportation, and room and board. Anticipate expenses.

- Make a savings plan: If you have a job and can save, or if you want to get one to help pay for your college fees, think about putting any extra money into a high-interest savings account to help it grow even more.

- Make adjustments: You now have a clear understanding of what more financial adjustments you need to make in light of your knowledge of how much money you have to spend, how much money you are borrowing, and how much money you can save.

READ ALSO: Restarting of Student Loan Interest on Friday: Here’s What You Need to Know